Ashtead Technology: The Offshore Bet You Haven't Made (Yet)

Where the Rig Meets the Reward

Ashtead Technology is a company that supports the installation, decommissioning, and IMR (inspection, maintenance, and repair) of offshore energy infrastructure by renting out equipment and technologies to the sector.

Overview

Ticker: AT

Market cap: £403 million

Share price: £5.01 / 501 pence

Founded: 1985

Headquarters: Westhill, Aberdeenshire, Scotland, United Kingdom

(Data accurate as of 09/03/2025)

Business Breakdown

So what does Ashtead actually do? To do almost anything significant in the offshore sector you need specialist equipment. Ashtead has an arsenal of equipment ranging from sensors to robotic equipment to winches. Basically, if you are in need of anything needed to install, decommission, or maintain/repair/inspect offshore energy infrastructure, then Ashtead are your guys.

By way of background, the offshore energy sector consists of two main subsectors: firstly, oil and gas, and secondly, renewables, primarily in the form of offshore wind. For decades, oil and gas was Ashtead’s bread and butter, and was the primary focus before the advent and rise in demand for renewables. Now, Ashtead’s revenue split between the two are:

Based on the 31 December 2024 results

You may be wondering why an offshore energy company would rent equipment from Ashtead rather than buy it for themselves. Specialist equipment usually has significant upfront purchase costs, and additional costs would be incurred when maintaining, repairing, and storing that equipment. This means that if companies rent the equipment from Ashtead instead of buying it themselves, they will only pay for it when they are utilising it, which can be cheaper in the long run. Moreover, if they need equipment at short notice, renting may be their only option, especially when you take into account that some equipment needs to be operated by specialist personnel, which Ashtead would provide. It is these advantages of renting which drive Ashtead’s business, and create its value proposition.

Moat

Ashtead benefits from its international scale. It has (a) customers across 80 countries, (b) has more than 23,000 rental assets, and (c) has hubs in the United Kingdom, Europe, the Americas, Africa, the Middle East, and the Asia Pacific. This means it benefits from economies of scale through cheaper equipment servicing, and more favourable pricing due to higher volume of equipment purchases.

Source: 2023 Results Presentation

Thesis

For background, the offshore rental equipment is highly fragmented. Since 2017, Ashtead has successfully acquired and integrated seven companies and has recently acquired two more (Seatronics and J2 Subsea). Acquisitions are part of Ashtead’s plan to deliver growth. Further acquisitions will expand its service offering and market share, thereby giving it further scale. It will also give Ashtead the opportunity to engage in cross-selling.

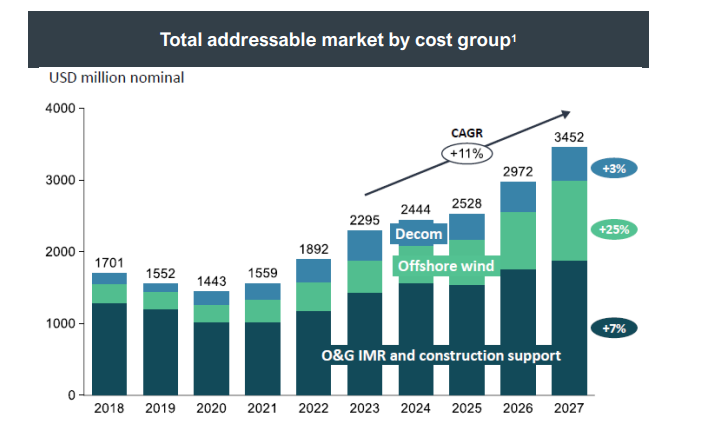

Another growth driver is the increasing global demand for energy. Both offshore renewables and oil and gas sectors (including decommissioning which Ashtead supports too) are projected to increase at an 11% compound annual growth rate. Ashtead is well poised to benefit from this as it supports companies in these sectors.

Source: 2023 Results Presentation

Skin the game

CEO, Allan Pirie, owns 1.6% of shares (worth circa USD 6m) and CFO, Ingrid Stewart, owns 0.4% of shares (worth circa $2.1m). While not massive insider-ownership, management has a sufficient shareholding for there to be an alignment of interests with shareholders.

Quick look at the numbers

You’d be forgiven for thinking something had gone terribly wrong with Ashtead’s business given the 30% fall in share price in the last year. However, since IPO both revenues and profits have grown year on year, with increases of 51% and 75% in revenue and net income respectively from FY22 and FY23. Moreover, the board have reiterated that full-year profit for FY24 is ahead of consensus expectations with unaudited revenues projected to be £168m (£110m – FY23), which means this positive momentum is set to continue.

In light of this, Ashtead Technology’s share price is attractively priced right now with a PE ratio of 20, a PEG ratio of only 0.26, and profit margins of around 78%. Consequently, the writer suggests this company is currently undervalued.

Other write-up

Check out this great write-up by ROIC2203 of Value Investors Club from 31 May 2024 on Ashtead Technology.